Introduction to Digital Banking – Delivery Channels | Customer Preferences | Information Security

- Blog|FEMA & Banking|

- 11 Min Read

- By Taxmann

- |

- Last Updated on 19 April, 2024

Latest from Taxmann

Digital Banking refers to the automation of traditional banking services through digital and online platforms, allowing customers to manage their finances without needing to visit a physical bank branch. This includes a wide range of activities such as transferring money, depositing checks, paying bills, managing investments, and accessing loans, all performed via websites or mobile applications. Digital banking is characterized by its convenience, speed, and availability, typically offering services 24/7. This shift towards digital platforms is driven by advancements in technology and changing consumer expectations, emphasizing efficiency and accessibility in financial services.

Table of Contents

- Introduction

- Need for Digital Channels

- Cost of Transactions

- Customer Preferences for Digital Banking

- Customer Digital Interface for Digital Banking Products

- Technology – the Foundation for User-Friendliness and Customer Interaction

- Security is the Cornerstone of Digital Banking

- Information Security (IS)

Check out IIBF X Taxmann's Digital Banking which is a comprehensive guide to the digital transformation in banking. It covers digital banking products, financial inclusion, marketing strategies, payment systems, and future trends like Blockchain and AI, making it an invaluable resource for students, professionals, and those interested in the digital banking revolution.

1. Introduction

Digital banking, internet banking, Omni Channel or online banking refers to using digital channels and technologies to conduct financial transactions and manage financial services.

Digital banking allows customers to access their bank accounts and perform banking transactions through a web-based or mobile applications. This includes checking account balances, transferring funds between accounts, paying bills, applying for loans and opening new accounts online.

With digital banking, customers can access their accounts and manage their finances anytime and from anywhere without visiting a physical bank branch. This provides convenience, flexibility and cost savings for the bank and the customer. Digital banking enables banks to offer their customers new and innovative services and products such as digital wallets, mobile payments and peer-to-peer transfers.

The term “digitization” describes the transition from analogue to digital implementations of certain tasks. Think about how far automated teller machines have come from when customers had to deal with a human teller to get their money out of the bank. As an organization undergoes a digital transformation, it unifies and streamlines its many digital components (such as digital operations, processes and other digitally enabled activities). Efforts like this aim to provide a unified customer experience across all channels and gain a comprehensive understanding of each individual client’s needs. Digital reinvention is pushing digitalization to new heights, which itself is developing.

Today, the world is fast-paced and financial processes run on the cutting edge of applied technologies. Large volumes of money must be moved instantaneously across the globe, or transactions are desired in the physical world without physical cash. Customers look towards completing their banking and other financial operations from the comfort of their homes and with maximum possible convenience. This has led to the advent, rise and explosion of Alternate Delivery Channels, quickly overtaking traditional Banking Channels like Brick-and-Mortar (i.e., branch-based) banking. Alternate Delivery Channels include ATMs, Debit/Credit/Prepaid Cards, Point of Sale (POS) terminals, Internet, Unified Payment Interface (UPI) and Mobile Banking. Also, advanced electronic payment systems like RTGS and NEFT have quickened and interlinked transactions across organisations and individual accounts. The Development and use of Alternate Delivery Channels contribute to digital banking.

Digital Banking is evolving using new innovative technologies and banking tools. It aims to leverage the strengths of digital technologies to bind and put together the standard online/mobile/electronic banking services to enrich and enhance the value of the service rendered and user experience. An example may be to run Analytics in the background. At the same time, the customer is online and controls the screen-based interactive content in the session to facilitate the customer’s banking activities while attempting ‘up sale’ or ‘loyalty enforcement’ for the bank. Customer centricity is a major trend in service industries now, and to do this in banking, banks need to capture customer actions in the banking application, and then process that huge data to yield meaningful insight into customer behaviour and needs and create services and products to meet them, market them where exactly customer expects them, etc. Using and leveraging digital techniques for this entire gamut is all that digital banking is about.

Conducting a banking business in the modern age would be extremely challenging without digitalization. Financial institutions that fail to provide adequate service to their clientele in this digital age will not fare well in today’s highly competitive financial environment. Nowadays, inhabitants staying in the farthest corners of the world can relate to the help of modern processes. Electronic banking services such as money transfers, statements, enquiries, deposit creation, online trading settlements, online actions, fees and taxes payments etc., are all made possible without visiting a bank. Banks, by examining the customer portfolio and transaction habits etc., quite often initiate payment reminders, analysis of investments, advisories on markets and many other financial conveniences. These can happen without physical travel or loss of time across accounts in various banks of the same or different customers. Digital Banking is more than just going paperless. Besides reducing paper-based transactions, the primary focus is enhancing the product suite with value-added services and achieving an integrated channel experience, through Omni Channel services, for the customer.

Banking operations have transformed from Manual Ledgers to Advanced Ledger Posting Machines (ALPMs) to Core Banking Systems (CBS) during the last two decades of the 20th century and the initial phase of the 21st century. CBS automated banking operations, where the customer has the option to do the same transaction, say payment, over multiple channels, viz. Cheque issuance/NEFT/IMPS/Card based payment, Fund Transfer through UPI/BHIM/Wallets etc., using either bank branch, Internet or mobile. Now, Banking is moving towards “Open Banking”, where banks open up their APIs (Application Programming Interfaces) for third parties to develop new apps and services. This service allows banks to offer more personalized products & services to their customers.

2. Need for Digital Channels

Due to the growing demand for increased consumer convenience, accessibility and banking options, alternative delivery channels are becoming increasingly important in today’s banking business. Some of the many benefits of using non-traditional methods of distribution include the following:

- Customers today want the convenience of checking their accounts and making financial transactions whenever and wherever they like. Online, mobile banking and UPI banking are three major alternative delivery channels enabling financial institutions to fulfil these needs.

- A traditional bank branch’s operating and maintenance costs can add up quickly. Alternative delivery channels help banks save cost with added advantage of enhanced customer convenience.

- Alternative delivery channels allow banks to serve consumers in locations where opening a branch would be too expensive or impractical.

- Customers can get a more tailored and hassle-free service using alternative delivery channels. Mobile banking apps, for instance, can furnish customers with individualized budgeting advice, specialized product recommendations and remuneration for their loyalty.

- Biometric verification, two-factor authentication and real-time fraud detection are some improved security features made available via alternative distribution channels.

- The convenience and adaptability that various distribution channels offer customers give banks an edge in today’s fast-paced, digital environment.

It is evident that both brick-and-mortar channels (branches) and ATMs are under pressure for banking services not only from the operations point of view but also from the business point of view. Besides this, the cost of performing a transaction at the bank branch level is quite high compared to ATM; the cost is further reduced when a customer opts to transact at a Merchant Point of Sale (PoS), E-commerce, or Mobile Banking. Incidentally, we have only 60.7 lakhs bank-linked POS devices (RBI Annual Report, 2021-22) and considering the population, this seems inadequate.

Adopting digital channels can help banks to cut costs, deepen customer satisfaction and loyalty, and drive long-term relationships and profitability.

3. Cost of Transactions

According to an ASSOCHAM-PwC study, Banks in India can reduce costs by up to 50 per cent on a per-transaction basis by redesigning their processes and systems for the digital age, structurally changing their cost base and instituting more aggressive ongoing cost management processes.

Banks incur cost in implementing and maintaining the infrastructure required for processing electronic transactions. They have both fixed and recurring costs which are incurred for ensuring that the infrastructure is safe and secure, and processing of payments is done in timely manner. Processing such transactions also involves costs as sufficient manpower/resources need to be deployed to support their processing.

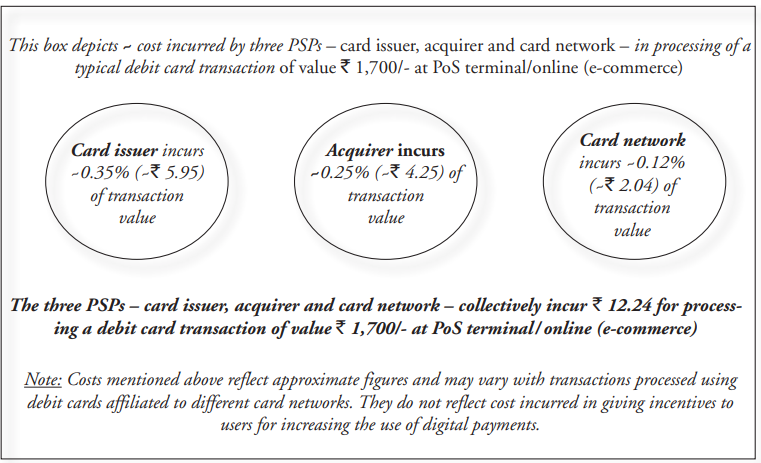

For transactions performed using a debit card, the costs incurred by the issuer are limited to the cost of IT systems, fraud risk management systems, support systems and incentives (like reward and loyalty points) for customers. Unlike in credit cards, the debit card issuer does not incur any cost on the funds transferred. It also enjoys the float benefit. In this regard, the transaction done using a debit card is akin to a normal funds transfer payment transaction, with deferred net settlement where the merchant receives the funds on a T+n basis. The below mentioned depicts the approximate cost incurred by stakeholders in processing a debit card transaction.

Box 1: Approximate cost incurred by PSPs in processing of a typical debit card transaction

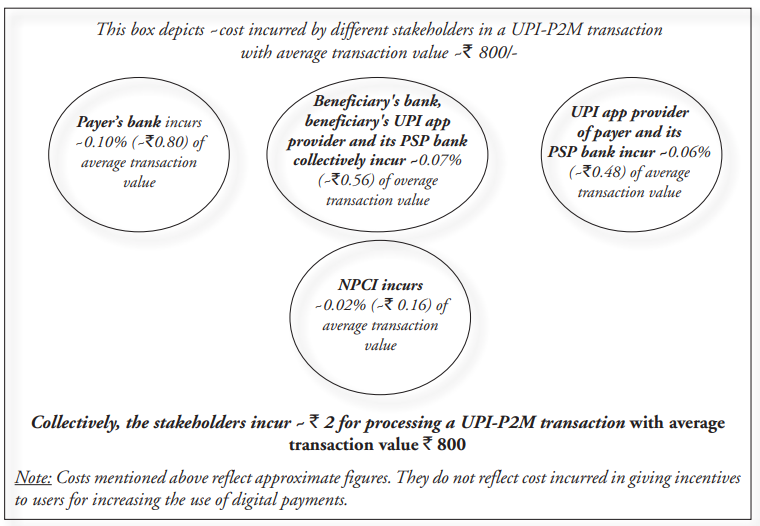

As on date, charges in UPI are nil for users and merchants alike. Merchant payments using UPI do not require installation of costly infrastructure by merchants as UPI QR codes are used. The cost of merchant infrastructure for UPI is lower as compared to the cost incurred in a card-based acceptance infrastructure. UPI as a fund transfer system enables real-time movement of funds. UPI as a merchant payment system also facilitates real-time settlement, as against the T+n settlement cycle for card settlements. However, the settlement among participant banks in UPI is on a deferred net basis. Facilitating this settlement requires the Payment System Operators (PSO) and banks to put in place adequate systems and processes to address the settlement risk. This involves additional costs to the system. The below mentioned chart depicts the approximate cost incurred by stakeholders in processing a UPI P2M transaction.

Source: Discussion Paper on Charges in Payment Systems, RBI

4. Customer Preferences for Digital Banking

The shift towards alternate delivery channels in banking has been occur- ring for some time, and it’s expected to continue in the coming years. Customers are increasingly using digital channels such as mobile banking apps, online banking and chatbots to conduct their banking activities, which is driving the growth of digital banking.

It is observed that customers do not mind having to pay a little extra for digital banking services, as it offers them value and convenience. The add-ons like e-wallets for loyalty points, social media notifications etc., are perceived as value-adds, and customers may not object to being charged for them.

Recent developments of new digital features in banking service delivery often utilise:

- Improvements in user-experience design through interactive interfaces that blur the boundaries between the real and the virtual, thereby, bringing data to life through rich presentations.

- The power to access the internet from anywhere.

- Tremendous advances in Analytical tools which can decipher and work out customer profiles.

- New technologies enable end-to-end communication between the customers and the Bank.

Relationship in banking is very important which ties a customer to the bank. A bank that can cater to customers’ requirements in a desired format, functionality, platform, speed and ease in the initial interactions is likely to be the bank of choice for customers when they are planning to buy another financial product. Incidentally, it is seen that while the elderly population do not change their banker easily and they refer all their needs to their existing bank first, the younger generation displays less loyalty and goes for the best deal in the market. So, customer retention for banks has become tougher, especially, in the case of young customers.

5. Customer Digital Interface for Digital Banking Products

Customers today look for high digital communication standards, sleek page designs, rich functionalities, rapid results for searches and interactive features. Digital banking permits the customer to generate their accounts statement from anywhere on a 24 × 7 basis instead of waiting for a monthly statement by postal mail.

Consumers today have a vast amount of information, a large amount of which is often obtained instantaneously. Opinions, both good and bad, can be shared in seconds and can even go viral. This is exemplified by various posts on Facebook, WhatsApp, Twitter and even email. Therefore, it is essential for banks to understand their contemporary customers well and take care of their changing needs, failing which there is every possibility of the customers turning around and becoming a source of bad publicity for the Bank.

Banks must understand the logic of customer thinking in deciding where to save their money and in choosing their primary banking relationship. This has a long-term influence on the customer, which can also strongly influence their friends and social circle.

There are some aspects that banks need to reckon with for offering robust digital services, namely:

- Customers’ attitude and behaviour are evolving rapidly.

- Digital mode is preferred worldwide.

- Digital technology is changing, and every technological advance opens new capabilities for enhancing customer experience.

- Technology reduces the cost of operations and servicing for the bank, and the reduction can, thereby, be passed on to the customer.

- Technology also reduces the delivery time of products/services.

- Digital channel is more customer friendly in terms of saving their effort, cost and time.

- However, computerised operations bring in their associated risks, and all products, services, and offerings must be secure so that information loss, error and unintended access do not happen. With more digital content and platforms, banks need to implement information security measures to protect interests of both Bank and Customer.

- Customer education and communication for technology-based services will be different in content and mode of delivery, compared to traditional practices. Banks need to master these also for effective use of their offerings.

6. Technology – the Foundation for User-Friendliness and Customer Interaction

Digital banking relationships need to move beyond basic internet banking to 360-degree interaction. In the digital era, KYC or ‘Know Your Customer’ is something beyond regulatory compliances and is trying to determine the complete customer profile and how the customer wants to interact with the bank. Tools such as data mining, analytics, etc. are being used to map customers’ behaviour, preferences and attitude.

With customers adopting more and more digital channels for communications, banks have a new opportunity to present themselves in a fresh light. Banks must understand and appreciate the evolving behavioural patterns in using bank accounts, purchasing lifestyle goods online, resorting to e-commerce etc. Getting it correct can reap rich rewards for banks in the long term, whilst getting it wrong can potentially lead to a lost generation of customers. It is very important to note here that the formulation of a digital banking service needs to take cognizance of the customer’s behaviour and needs based on his/her habits and general practices in society. For example, say a young customer is comfortable on Facebook or similar social media for a longer part of his time and displays tendencies to use advertisement links and hints to search and make online purchases or searches for banking services. A bank’s presence in such a platform, look and feel of the offerings, ease of navigation of the options offered for transaction, stability and security of its operations thereon will be found helpful for that customer, if the bank’s messages and navigations are aligned to such environment and user behavioural aspects. Understanding the customer and aligning and empowering services are the basic steps at the backend of digital banking.

7. Security is the Cornerstone of Digital Banking

Security extends from the bank’s hardware to the endpoint devices – whether a PC/Mac at home, a tablet or the newest smartphone. In all cases, digital banking must employ strong and secure technologies which protect communication, user information and the bank’s IT infrastructure.

Banks should address weaknesses in security, balance between security posture and business goals and also think beyond regulatory compliance.

The most common issues that banks need to address to achieve effective and proactive security in their digital banking segments are:

- Linking security and business practices – Dovetailing.

- Robust Information Security Governance – Prescribing best practices and controls in development, operations and delivery of services; Customer education and effective Information Security Audit procedure.

- Engaging business stakeholders in the security dialogues.

- Aligning IT Governance with business goals of the organisation.

- Governing the enterprise – Establishing appropriate frameworks, policies and controls to protect IT environments and practice info-security.

- Establishing an effective Cyber Security Operations Centre (Cyber S.O.C)- Keeping pace with persistent threats – Adopting a proactive and dynamic approach, including intelligence, analytics and tie-up with specialized security service providers to deal with the widening array of possible failures/attacks.

- Addressing the security capability need – Developing, training and retaining staff experienced in security planning, design and execution to increase the likelihood of continued success of the security set-up.

In the following chapters, we shall look at various aspects of digital technology-based banking operations, different products, channels, and the issues involved.

8. Information Security (IS)

All actions and values of the bank, customers, and vendors, like customer data, transactions, business data etc., are recorded electronically in the bank’s computer system. Information Security is the domain of knowledge and practices to secure this information. Information Security (IS) is designed to protect the confidentiality, integrity and availability of computer system data from those with malicious intentions. Cornerstone of Information Security is the concept of protecting the CIA-Confidentiality, Integrity and Availability – for both Bank and its customers.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.

Taxmann Publications has a dedicated in-house Research & Editorial Team. This team consists of a team of Chartered Accountants, Company Secretaries, and Lawyers. This team works under the guidance and supervision of editor-in-chief Mr Rakesh Bhargava.

The Research and Editorial Team is responsible for developing reliable and accurate content for the readers. The team follows the six-sigma approach to achieve the benchmark of zero error in its publications and research platforms. The team ensures that the following publication guidelines are thoroughly followed while developing the content:

- The statutory material is obtained only from the authorized and reliable sources

- All the latest developments in the judicial and legislative fields are covered

- Prepare the analytical write-ups on current, controversial, and important issues to help the readers to understand the concept and its implications

- Every content published by Taxmann is complete, accurate and lucid

- All evidence-based statements are supported with proper reference to Section, Circular No., Notification No. or citations

- The golden rules of grammar, style and consistency are thoroughly followed

- Font and size that’s easy to read and remain consistent across all imprint and digital publications are applied