[Analysis] FDI in India – Country-Wise Distribution | Entry Routes | Sectoral Caps

- Blog|FEMA & Banking|

- 9 Min Read

- By Taxmann

- |

- Last Updated on 25 October, 2024

Latest from Taxmann

FDI (Foreign Direct Investment) in India refers to the investment made by a non-resident entity or individual into the equity or capital of an Indian company. It allows foreign investors to establish or acquire a business in India, either through the automatic route (where no prior government approval is required) or the government route (which requires approval). FDI plays a crucial role in India's economic growth, contributing to sectors like IT, manufacturing, financial services, and more. India has eased FDI norms across various sectors to attract foreign investments, promoting industrial development and job creation.

Table of Content

- Statistics

- India Entry Strategy – Market Penetration

- Entry Routes for Foreign Entity in India

- Comparative Analysis – Type of Business in India

- LO/BO/PO – Purpose for Setting Up in India

- Different Entity Incorporation in India

- Foreign Direct Investment in India

- Entry Routes

- Sectoral Caps

- Wholly Owned Subsidiary or Joint Venture

- Limited Liability Partnership (LLP)

- Prohibited Sectors

- Taxation Overview in India

- Case Study

1. Statistics

* Source: RBI

- Foreign Associate Companies: if a non-resident investor owns at least 10% and no more than 50% of the voting power/equity capital

- Foreign Subsidiary Companies: if a non-resident investor owns more than 50 per cent of the voting power/equity capital.

1.1 FDI in India – Country Wise Distribution (2024)

| Country | Amount (In Crore) | Percentage |

| USA | 10,11,972 | 16.70% |

| Mauritius | 9,09,403 | 15.00% |

| Singapore | 8,40,685 | 13.90% |

| UK | 7,24,958 | 12.00% |

| Netherlands | 5,61,331 | 9.30% |

| Japan | 5,42,522 | 9.00% |

| Switzerland | 4,02,399 | 6.60% |

| Germany | 2,20,356 | 3.60% |

| France | 1,52,393 | 2.50% |

| South Korea | 1,06,918 | 1.80% |

| Others Countries | 5,84,662 | 9.60% |

* Source: RBI

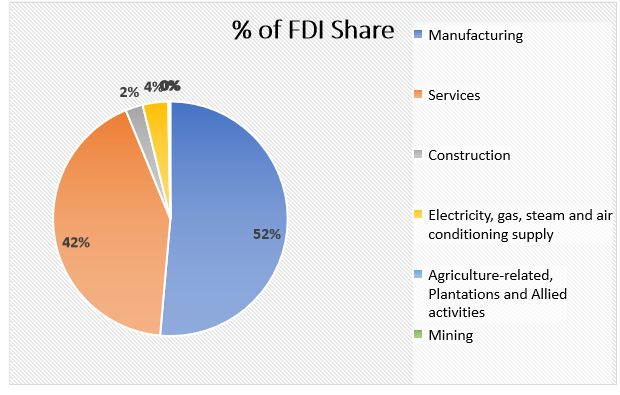

1.2 Sectors Attracting Highest Inflow (2024)

2. India Entry Strategy – Market Penetration

Market Analysis & Expansion

- Market Mapping, Market Sizing

- Competitive Analysis

- Regulatory Overview

- Feasibility Study of Setting up India Business

- Opportunity to increase sales or expand their business

JV & Partnership

- Strategic Investment and partnership

- Identification of JV Partners and Strategic Alliances

- Identification of Acquisition Targets

Channel Partners & Policy Reforms

- Identification of Potential Vendors

- Channel Study and Identification Channel partners

- Various government incentives to attract foreign Investment

Site Analysis & Talent Pool

- Manufacturing Site Analysis

- Human Resource Study including Costs, Benchmarking, Availability, sourcing

- Talent Search and Team Building

3. Entry Routes for Foreign Entity in India

For carrying out manufacturing/services and other related business operations

Indian Company*

- Joint Venture

- Wholly owned Subsidiary

OR

Limited Liability Partnership

- LLP

OR

For carrying out EXIM, Research and project execution operations

Foreign Company**

- Liaison Office

- Branch Office

- Project Office

X

Partnership Firm

- Partnership

One Person Company

- OPC

*Incorporate company in India s.t. sectoral caps and requisite approvals

**As per company law, a resident having PAN to be appointed for receiving notices in India for foreign company

4. Comparative Analysis – Type of Business in India

| Private Company vis-à-vis Public Company vis-à-vis OPC vis-à-vis LLP | ||||

| Particulars | Private | Public | OPC | LLP |

| Min Members | 2 | 7 | 1 | 2 partners |

| Max Members | 200 | Unlimited | 1 | No Limit |

| Min Directors | 2 | 3 | 1 | 2 Designated Partners |

| Max Directors | 15* | 15* | 15* | NA |

| Resident Director | 1 Mandatory | 1 Mandatory | 1 Mandatory | 1 Designated Partner |

| Transfer of

ownership |

Ownership can be Transferred | Ownership can be transferred | Ownership can be transferred to nominee in the event of death of owner | Ownership can be transferred |

| Subscription of shares | Public subscription not allowed | Public subscription allowed | Public subscription not allowed | Public subscription not allowed |

| Issue of Prospectus | Not Mandatory | Mandatory | Not Mandatory | Not Mandatory |

| Managerial Remuneration | No limit for managerial personnel | Shareholder approval is required, If remuneration payable is above limits | NA | Remuneration is based on LLP agreement |

| Commencement of Business/Operations | Declaration to be filed prior to commencement | Declaration to be filed prior to commencement | Declaration to be filed prior to commencement | Immediately after obtaining certificate of incorporation |

|

Legal Status |

Pvt Co is a separate legal entity registered under Companies Act, 2013. The Directors are liable for defaults made under the act |

Public Co is a separate legal entity registered under Companies Act, 2013.

The Directors are liable for defaults made under the act |

OPC is a separate legal entity registered under Companies Act, 2013.

The Directors are liable for defaults made under the act |

LLP is a separate legal entity registered under LLP Act, 2008. The Designated partners of LLP are liable for contraventions under the act |

| Governing Act/Law | Companies Act, 2013 | Companies Act, 2013 | Companies Act, 2013 | LLP Act, 2008 |

| Annual Statutory Filings | Annual statement of accounts & annual return with ROC | Annual statement of accounts & annual return with ROC | Annual statement of accounts & annual return with ROC | Annual statement of solvency & annual return with ROC |

| Annual Filings & Audit | IT return to be filed. Audit mandatory | IT return to be filed. Audit mandatory | IT return to be filed . Audit mandatory. | IT return to be filed. Audit mandatory in case turnover exceeds INR 40 lakhs or contribution exceeds INR 25 lakhs |

Note: Resident Director: sec 149(3) – Every company should have at least one director who has stayed in India for a total period of not less than 182 days in the Financial Year

5. LO/BO/PO – Purpose for Setting Up in India

Liaison Office

- Act as channel of communication between the Parent and Indian Company

- Promote Business and Product awareness

- Facilitate technical or financial collaboration

- Conduct Market research and gather information on Indian Markets

- Representing Parent company in India to handle Public relations.

Branch Office

- Conduct business operations and generate Income within India.

- Acts as extension of Parent company, providing the same products and services as the Parent company.

Project Office

- Execute and manage specific projects in India

- Typically set up for a limited period and is linked to the completion of a particular project.

- Bring expertise and skills for project implementation.

6. Different Entity Incorporation in India

| Particulars |

Liaison Office (LO) |

Branch Office (BO) | Project Office (PO) | WOS/JV |

LLP |

| Permitted activities

|

|

|

|

All types of business activities are permitted, such as in the manufacturing, marketing, services sectors

|

The LLP’s structure and objective are primarily suited for carrying out business activities related to the services sector

|

| Eligibility

|

|

|

NA | There is no minimum capital required for incorporating a private limited company | No minimum capital requirement conditions |

| Validity

|

Generally for 3 years* except in the case of NBFCs and those entities engaged in construction and development sectors, for whom the validity period is 2 years only

|

NA | As per the tenure of the project

|

A company, once incorporated, will continue until its dissolution

|

An LLP once incorporated continues till it is dissolved or as per terms stated in the LLP agreement |

| Prior Approval

|

RBI approval before commencement of any operations

|

RBI approval before commencement of any operations

|

RBI approval before commencement of any operations

|

Automatic or Government route

|

FDI is permitted under the automatic route

|

| Setup Timeline |

6-8 weeks |

6-8 weeks | 4 weeks | 4-8 weeks | 4-6 weeks |

| Tax Rate | Not subject to taxation in India | 40% | 40% | 25% |

30% |

| Annual Filing

|

Annual Activity Certificates (AAC) | Annual Activity Certificates (AAC) | Annual Activity Certificates (AAC) | FCGPR, FLA, FCTRS AOC 4 and MGT 7 | LLP 1, FLA Form 11 and Form 8 |

| Winding Up | Application for closure to AD-I Bank | Application for closure to AD-I Bank | Application for closure to AD-I Bank | NCLT order Companies Act | NCLT order Companies Act |

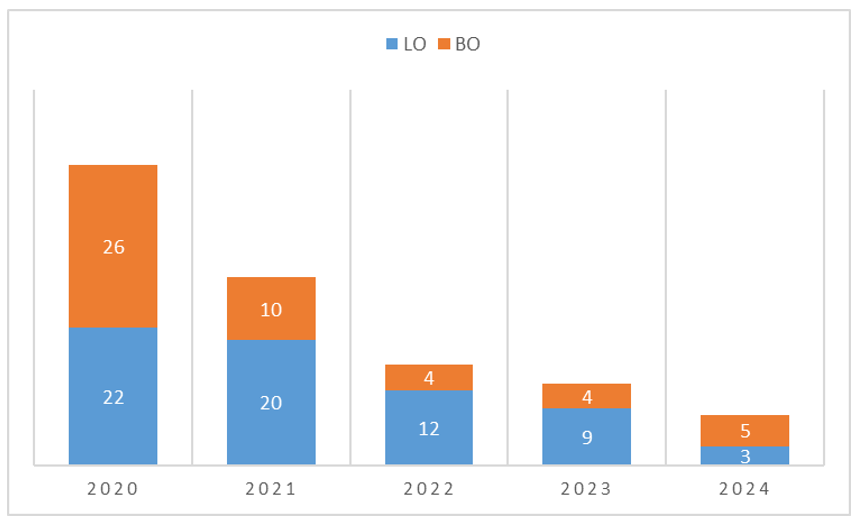

6.1 Statistics – LOBOPO

7. Foreign Direct Investment in India

Investment in India has improved considerably since the opening up of the economy in 1991. This is largely attributed to ease in FDI norms across sectors of the economy. India, today is a part of top 100 club on Ease of Doing Business (EoDB) and globally ranks 1st in the greenfield FDI ranking. India received the record FDI of $ 60.1 bn in 2016-17.

- Category 1: 100% FDI permitted through Automatic route

- Category 2: 100% FDI permitted through Government route

- Category 3: Upto 100% FDI permitted through Government + Automatic route

- Category 4: Upto 51% FDI permitted through Government/Automatic route

Note: In sectors/activities not listed above, FDI is permitted up to 100% on the automatic route, subject to applicable laws/regulations; security and other conditions.

8. Entry Routes

Routing Investments in India

8.1 Automatic Route

No prior approval from the Government of India is required.

- Available for most sectors, except those specifically restricted.

- Limits: Sectoral caps/stipulated sector-specific guidelines.

- Investors only need to inform the Reserve Bank of India (RBI) within 30 days of investment.

- Faster process since it bypasses government scrutiny.

8.2 Government Route

Prior approval from the Government of India is mandatory.

- Only for cases other than Automatic Route and those mentioned in sectoral policy.

- Investors must obtain permission from the concerned ministry or department before investing.

- An entity of a country, sharing land border with India or where the beneficial owner of an investment into India is situated in or is a citizen of any such country (Pakistan)

9. Sectoral Caps

9.1 Automatic Route (Illustrative)

- Mining

- IT

- Financial services(a)

- Construction Development

- Infrastructure

- Manufacturing sector

9.2 Government Route (Illustrative)

- Titanium (Mining) 100%

- Broadcasting (Content) 46%

- Banking for Public 20%

- Print 26%

- Insurance (a) 70%

9.3 Negative List (Illustrative)

- Agriculture(b)

- Atomic energy

- Lottery, betting and gambling

- Chit fund, Nidhi company

- Trading in Transferable Development Rights

- Cigars & Cigarettes

Note: (a) Sector-specific guidelines

(b) Subject to certain exceptions

10. Wholly Owned Subsidiary or Joint Venture

10.1 Wholly Owned Subsidiary

- Wholly Owned Subsidiary (WOS) can be set up in sectors where 100% foreign direct investment is permitted under the FDI policy. It can be set up by the Foreign Companies only.

- It operates as an independent legal entity whose 100 percent equity shares are owned by another company, the parent company.

- It can be in form of private company or public company.

- It carries out the business activities as a separate legal entity however controlling interest vest with the foreign parent Company.

- Profits can be taken out of India, net of Indian taxes, in the form of dividend.

- The WOS will be subjected to Indian taxes and laws as applicable to other domestic companies

10.2 Joint Venture

- A joint venture is a partnership between two or more companies or individuals who agree to pool capital or goods to run a business or to achieve a commercial objective

- It can be in the form of companies, partnerships or joint working agreements/strategic alliances.

- Foreign Companies set up Joint ventures in India in sectors where 100 percent FDI is not permitted

- JV helps foreign companies to utilize the existing networks of their Indian partners, and once taxed, such companies can remit their Indian profits outside the country.

- Corporate JVs will also be subject to the country’s tax laws, FEMA, labor laws, the Competition Act of 2002, and various industry-specific laws.

11. Limited Liability Partnership (LLP)

- LLP Firms are partnership firms with limited liability of partners. It is a combination of partnership and a Company

- 100% Foreign Direct Investment in LLP is allowed for the sectors/activities where 100% FDI is allowed under the automatic route and there are no FDI-linked performance conditions.

- LLPs can also make downstream investment in another company or LLP in sectors where 100% FDI is allowed under automatic route.

- FDI in an LLP under the automatic route is subject to the following conditions:

-

- The LLP should come under a sector that has no FDI-linked performance conditions, which refers to sector-specific conditions for companies receiving foreign investment;

- The LLP should be in a sector that permits 100 percent FDI; and

- The conditions of the LLP Act of 2008 and rules thereunder are met

12. Prohibited Sectors

- Lottery Business including Government/private lottery, online lotteries, etc.*

- Gambling and Betting including casinos*

- Chit funds

- Nidhi Company

- Trading in Transferable Development Rights (TDR)

- Real Estate Business or Construction of farmhouses**

- Manufacturing of cigars, cheroots, cigarillos and cigarettes, of tobacco or of tobacco substitutes

- Sectors not open to private sector investment- atomic energy, railway operations (other than permitted activities mentioned under the Consolidated FDI policy)

Notes

*Foreign technology collaboration in any form including licensing for franchise, trademark, brand name, management contract is also prohibited for Lottery Business and Gambling and Betting activities

**Real estate business shall not include development of town shops, construction of residential/commercial premises, roads or bridges and Real Estate Investment Trusts (REITs) registered and regulated under the SEBI (REITs) Regulations, 2014

13. Taxation Overview in India

Key Features of India’s taxation System: Taxes in India are levied by the Central Government and the State Governments. Some minor taxes are also levied by the local authorities such as the Municipality and Local Government.

Major Central Taxes

- Income Tax

- Central Goods & Services Tax (CGST)

- Integrated GST (IGST)

- Custom Duty

Major State Taxes

- State Goods & Services Tax (SGST)

- Stamp Duty & Registration

A resident company is taxed on its worldwide income. A non-resident company is taxed only on income that is received in India, or that accrues or arises, or is deemed to accrue or arise, in India. Company whether Indian or foreign is liable to taxation, under the Income Tax Act, 1961. Corporation tax is a tax which is levied on the incomes of registered companies and corporations. Taxes In India are primarily into 2 categories:

- Direct Tax

- Indirect Tax

14. Case Study

Non-Resident to convert Partnership firm into WOS

Facts of the case:

- An Foreign Company “XYZ Ltd” into Pharma Industry wanted to acquire Delhi based Partnership firm via Equity Capital.

- Delhi-based firm was into manufacturing of Daily Home care essentials.

Questions:

- Is this transaction allowed under FEMA?

- Can NR invest in Partnership firm?

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.