[Analysis] Evolution of Sustainability Reporting in India – Understanding the Impact and Implications

- Blog|Account & Audit|

- 9 Min Read

- By Taxmann

- |

- Last Updated on 11 September, 2024

Latest from Taxmann

The BRSR (Business Responsibility and Sustainability Report) Framework is a regulatory guideline mandated by the Securities and Exchange Board of India (SEBI) for top-listed companies in India. This framework, which evolved from the earlier Business Responsibility Report (BRR), aims to enhance transparency and accountability in reporting the non-financial disclosures of companies, focusing on their environmental, social, and governance (ESG) initiatives. The implementation of the BRSR is part of a global trend towards integrated reporting, reflecting the increasing importance of sustainability issues in the corporate and financial sectors.

Table of Contents

- Introduction

- History of Sustainability Reporting in India

- Business Responsibility and Sustainability Report

- Nine Principles of the NGRBCs

- ESG Audit

- Conclusion

1. Introduction

The term “Sustainability Reporting” encompasses the practice of disclosing the economic, environmental, and social impacts of an organization’s everyday operations. This type of reporting is crucial as it provides stakeholders with a clear insight into the organization’s contributions toward sustainable development.

Recognizing the importance of accurate and transparent disclosures, sustainability reporting has gained global acceptance. Nations such as the United Kingdom, the United States, and China have made it mandatory for companies to prepare these reports. India, aligning with global standards, has introduced a requirement under the Environmental, Social, and Governance (ESG) framework termed the “Business Responsibility and Sustainability Report” (BRSR). The top 1000 listed entities in India are now required to issue a BRSR along with their annual reports, detailing their performance against the nine principles of the “National Guidelines on Responsible Business Conduct” (NGRBC).

2. History of Sustainability Reporting in India

The journey towards formalized sustainability reporting in India began in 2009 when the Ministry of Corporate Affairs (MCA) issued Corporate Social Responsibility Voluntary Guidelines to steer businesses toward sustainable practices. In July 2011, the scope was broadened with the “National Voluntary Guidelines on Social, Environmental, and Economic Responsibilities of Business,” which outlined comprehensive principles for businesses to integrate into their operations.

In 2012, the Securities and Exchange Board of India (SEBI) mandated that the top 100 listed companies by market capitalization file a Business Responsibility Report (BRR), a requirement that expanded to the top 500 listed companies in 2017. The year 2019 marked a significant advancement in this area when the MCA formulated the National Guidelines on Responsible Business Conduct (NGRBC), and SEBI ruled that the annual reports of the top 1000 listed entities must include a “Business Responsibility Report”. This progression culminated in the SEBI notification dated 5th May 2021, which introduced the comprehensive reporting requirement under ESG through the BRSR framework.

3. Business Responsibility and Sustainability Report

The Business Responsibility and Sustainability Report (BRSR) requires listed entities to disclose their performance in alignment with the nine principles of the National Guidelines on Responsible Business Conduct (NGRBCs). Designed to enable comparability across different companies’ sectors, the BRSR mandates quantitative and standardized disclosures centred on environmental, social, and governance (ESG) parameters over time. The structure of reporting for each of these nine principles includes categories of essentials and leadership indicators.

Previously, compliance with the BRSR guidelines was optional until the end of the financial year 2021-22. Starting from the financial year 2022-23, however, it has become a mandatory requirement. According to the format outlined by the Securities and Exchange Board of India (SEBI), the disclosures in the report are organized into three main sections:

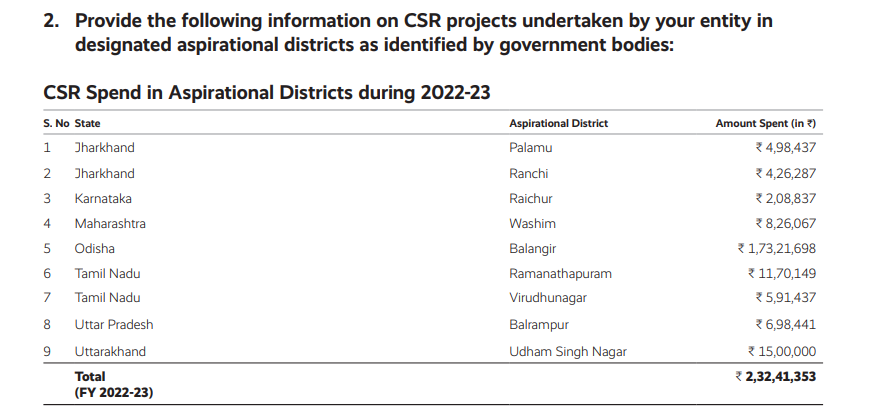

- Section A: General Disclosures – This section requires companies to provide general information, including basic details about the organization, such as its scale, size, sector, products, and employee strength. It also includes information on Corporate Social Responsibility (CSR) initiatives. Additionally, this section addresses the company’s operations in relation to environmentally sensitive areas, including proximity to protected zones and areas critical for social reasons, such as regions facing water scarcity.

- Section B: Management and Process – In this part of the BRSR report, the focus is on the organization’s commitment to principles of business responsibility. It involves disclosures regarding the governance framework, policies, procedures, and processes that conform to the principles of NGRBCs. This section aims to provide insights into the managerial infrastructure and the ethical commitments of the organization.

- Section C: Principle-wise Performance – This section details the organization’s performance relative to each of the nine NGRBC principles and their core elements. It showcases how the organization plans to uphold its commitment to conducting business sustainably.

Organizations have the option to report under two categories: “Essential” or “Leadership.” Choosing the “Essential” option means the organization reports the minimum required information necessary for compliance with responsible business conduct. The “Leadership” option allows organizations to report additional voluntary actions they have undertaken that go beyond the basic requirements, highlighting their leadership in sustainability and responsibility.

4. Nine Principles of the NGRBCs

The Business Responsibility and Sustainability Report (BRSR) is designed around the nine principles established by the National Guidelines on Responsible Business Conduct (NGRBCs), which are further supported by a guidance note to assist companies in understanding the required scope of disclosures for each principle. These principles are organized under the three categories of Environmental, Social, and Governance (ESG), with each category addressing specific aspects of responsible business conduct. Here’s a detailed discussion of each principle:

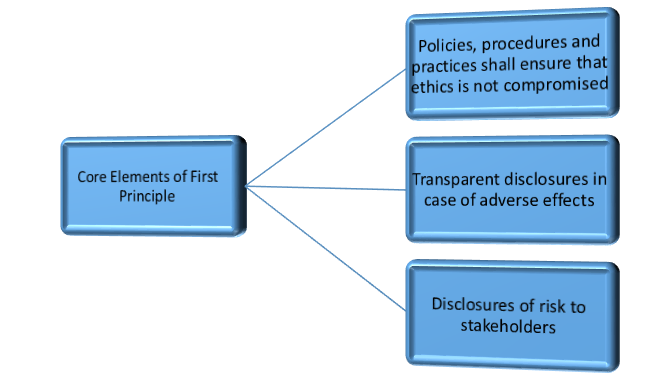

Principle 1 – Ethics, Transparency and Accountability

The organization is expected to conduct its business with integrity, operating in an ethical, transparent, and accountable manner. The practices adopted by the company should be robust, featuring well-defined roles and responsibilities to prevent conflicts of interest and ensure accountability at all levels. This principle champions a corporate culture where businesses are responsible not only to their shareholders but also to the broader community. It emphasizes the importance of avoiding corruption and cultivating a culture of trust across all business dealings.

The following extract from the annual report of a listed company outlines its compliance with the requirements of Principle 1:

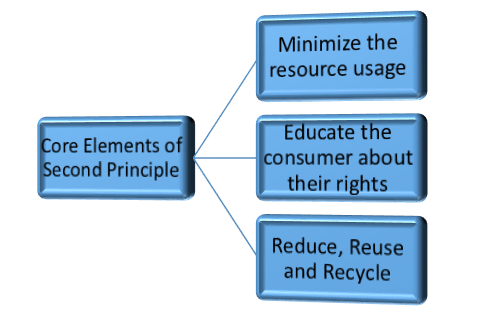

Principle 2 – Safe and Sustainable Goods and Services

This principle advises organizations to concentrate on creating and providing safe and sustainable goods and services. This principle promotes innovation and the development of products and services that not only minimize environmental impacts but also prioritize customer safety. It encourages businesses to integrate sustainability into their core operations, ensuring that their offerings are both environmentally friendly and safe for consumers.

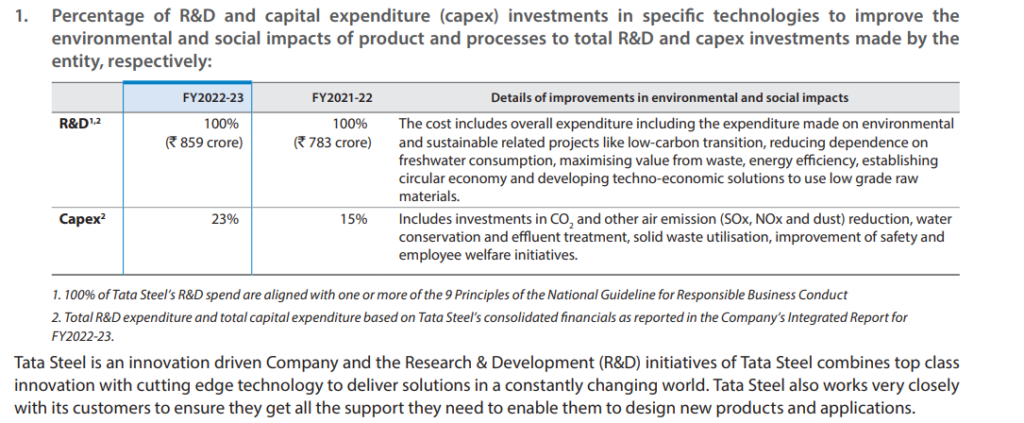

The following extract from the annual report of a listed company outlines its compliance with the requirements of Principle 2:

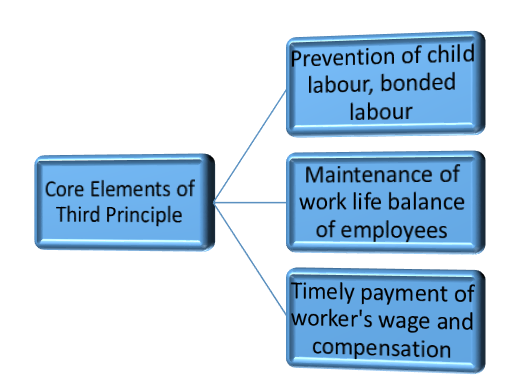

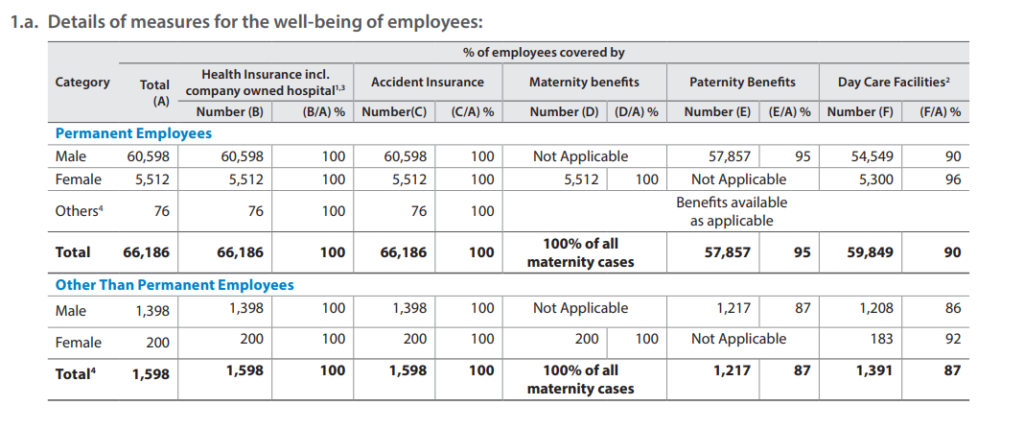

Principle 3 – Promote the Well-being of all Employees

This principle prioritizes the well-being of employees and everyone involved in the value chain by emphasizing the necessity of fair wages, decent working conditions, and social protection. It also aims to eradicate child labour and forced labour, requiring organizations to adhere to labour laws and ensure health and safety standards in the workplace. This principle advocates for a supportive and secure working environment that upholds the dignity and rights of all workers.

The following extract from the annual report of a listed company outlines its compliance with the requirements of Principle 3:

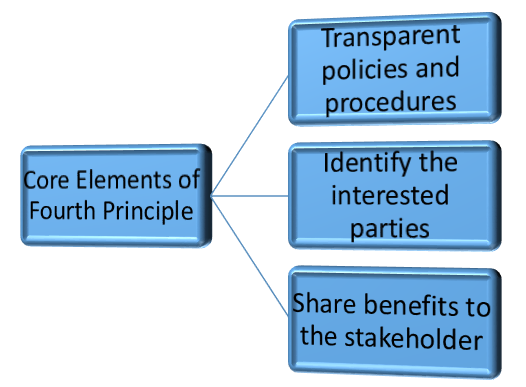

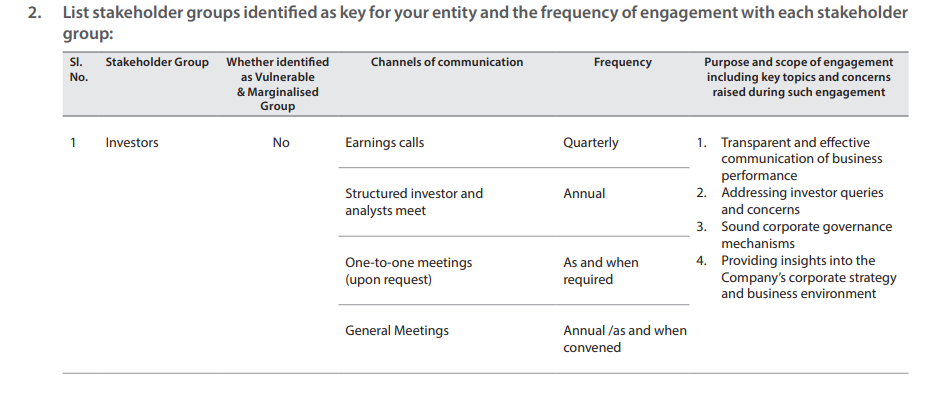

Principle 4 – Respect for Stakeholder’s Interest and Responsiveness

This principle emphasizes the importance of active engagement with stakeholders, urging organizations to listen to their concerns and consider their interests in decision-making processes. Organizations are also expected to maintain transparency, keeping stakeholders informed about how their operations and business decisions impact people and the environment. Additionally, this principle encourages businesses to fairly and transparently balance the occasionally conflicting needs of various stakeholders, ensuring that no group is disproportionately disadvantaged or overlooked.

The following extract from the annual report of a listed company outlines its compliance with the requirements of Principle 4:

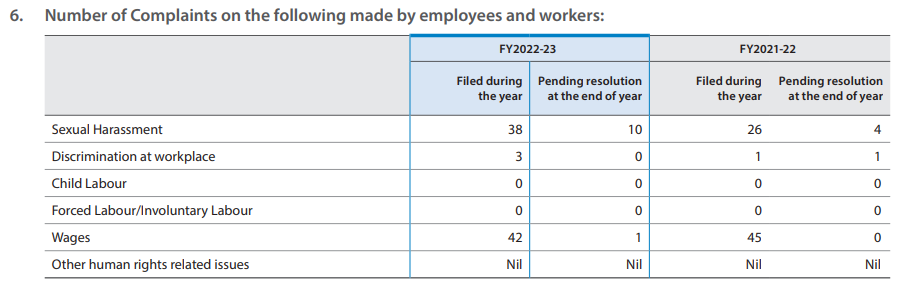

Principle 5 – Respect and Promote Human Rights

This principle addresses human rights concerns that arise directly or indirectly from business operations. Organizations are required to acknowledge and respect human rights in accordance with international standards, ensuring that their activities do not harm individuals or communities. This includes preventing discrimination, promoting equality, and safeguarding the dignity of all those affected by their operations. Additionally, this principle underscores the obligation of businesses not only to refrain from violating human rights but also to actively advocate for them within their sphere of influence.

The following extract from the annual report of a listed company outlines its compliance with the requirements of Principle 5:

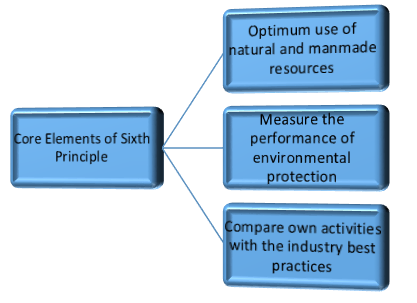

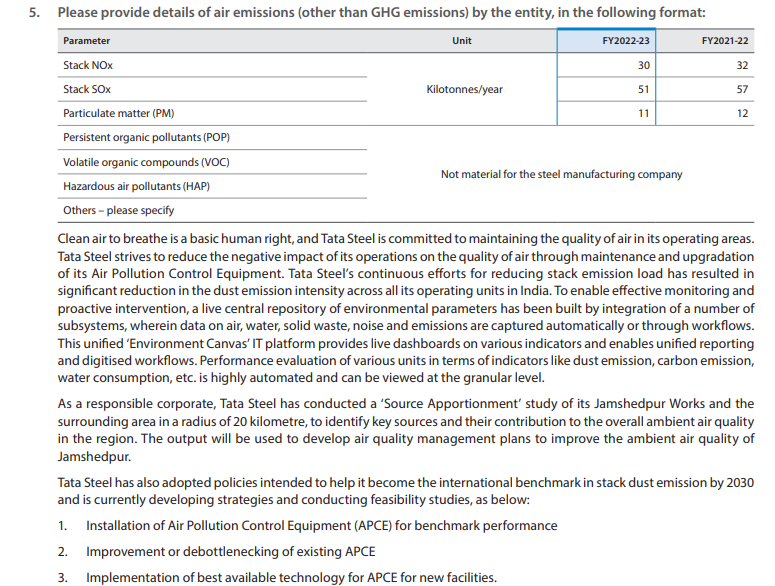

Principle 6 – Protection and Restoration of Environment

The organization should establish policies, procedures, and practices to assess and mitigate the environmental impacts caused by their business activities. They should also evaluate the environmental risks linked to their operations and implement measures to reduce these risks. Moreover, this principle promotes the restoration of ecosystems that have been damaged by business operations, emphasizing a commitment to protecting and preserving biodiversity.

The following extract from the annual report of a listed company outlines its compliance with the requirements of Principle 6:

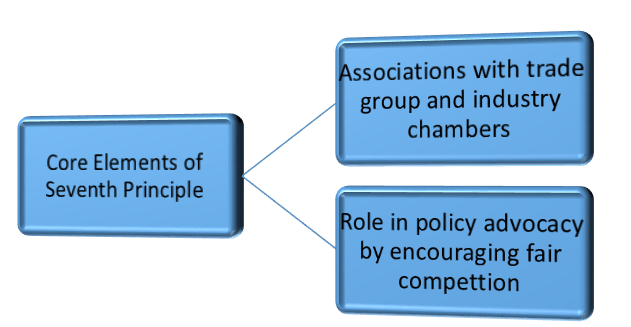

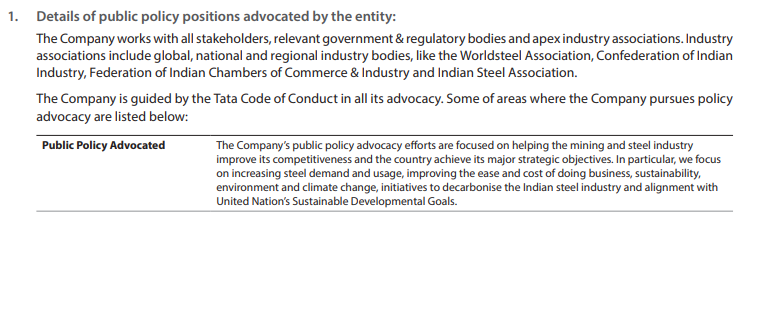

Principle 7 – Influence on Public and Regulatory Policies

This principle of the Business Responsibility and Sustainability Report (BRSR) emphasizes ethical engagement in influencing public and regulatory policies. Businesses are encouraged to ensure their actions are transparent and aligned with the public interest. This principle calls for organizations to integrate the core elements of BRSR comprehensively into their policy-making processes. It advocates for the promotion of policies that serve the public good rather than pursuing actions that benefit only their own interests.

The following extract from the annual report of a listed company outlines its compliance with the requirements of Principle 7:

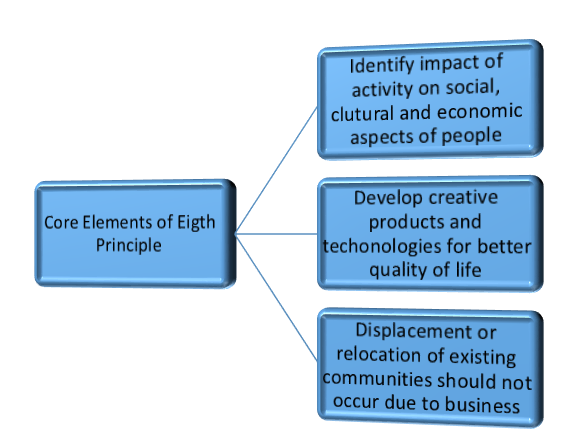

Principle 8 – Promote Inclusive Growth and Equitable Development

To promote inclusive growth and equitable development, the eighth principle emphasizes the need for collaboration among various stakeholders, including government bodies, businesses, and civil associations. This principle advocates for a unified approach where all parties work cohesively to improve livelihoods and support marginalized communities. Additionally, it calls for organizations to actively monitor, evaluate, and document the negative impacts of their activities on society and the environment. Based on these assessments, they must develop and implement action plans to effectively mitigate these impacts, ensuring progress towards inclusive and equitable growth.

The following extract from the annual report of a listed company outlines its compliance with the requirements of Principle 8:

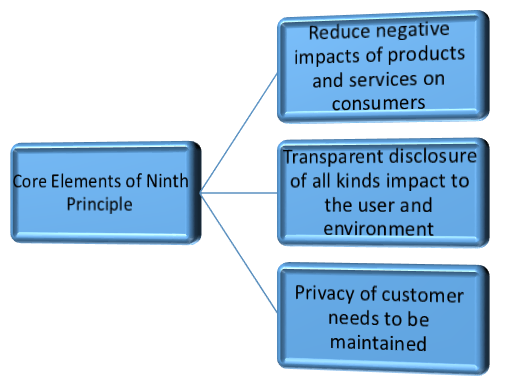

Principle 9 – Provide Value to Consumer in a Responsible Manner

This principle underscores that the fundamental objective of any business is to offer valuable products or services to customers while earning reasonable profits. It stresses the importance of responsible conduct in all consumer interactions, ensuring product safety and reliability, and providing truthful information with fair pricing. This principle also mandates prompt and transparent handling of consumer complaints. Moreover, it advocates for ethical marketing practices and the eradication of deceptive advertising, thereby fostering trust and loyalty among customers by prioritizing their best interests.

The following extract from the annual report of a listed company outlines its compliance with the requirements of Principle 9:

5. ESG Audit

Currently, the Securities and Exchange Board of India (SEBI) mandates that only the top 1000 listed companies integrate the Business Responsibility and Sustainability Report (BRSR) with their annual reports. However, it is anticipated that this requirement will soon be extended to other listed and unlisted companies. Given that the BRSR provides crucial sustainability-related information, the assurance of such reports is essential. This need for assurance will lead to the emergence of ESG (Environmental, Social, and Governance) audits.

An ESG audit is a process designed to help companies evaluate the environmental and social risks associated with their products, services, and operations. Additionally, it aims to assist businesses in reviewing risks in their supply chains, enhancing risk management capabilities, and improving transparency with stakeholders.

In response to the growing necessity for BRSR report assurance, the Institute of Chartered Accountants of India (ICAI) has issued the Standard on Sustainability Assurance Engagements (SSAE) 3000, which pertains to Assurance Engagements on Sustainability Information. This standard provides a framework for assurance engagements on an entity’s sustainability information.

It is important to note the following effective dates for the application of SSAE 3000: a) On a voluntary basis for assurance reports covering periods ending on 31st March 2023. b) On a mandatory basis, assurance reports cover periods ending on or after 31st March 2024.

6. Conclusion

The evolution of sustainability reporting in India demonstrates an increasing commitment to transparency and responsible business practices. By adhering to the nine National Guidelines for Responsible Business Conduct (NGRBC) principles, Indian businesses are positioned to achieve sustainable development. For listed entities, adopting the Business Responsibility and Sustainability Report (BRSR) framework extends beyond compliance with regulatory requirements. It represents a significant opportunity to showcase their dedication to ethical and sustainable practices. This commitment not only fosters long-term value creation but also enhances societal well-being, marking a crucial step forward in the integration of sustainability into core business strategies.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.

Taxmann Publications has a dedicated in-house Research & Editorial Team. This team consists of a team of Chartered Accountants, Company Secretaries, and Lawyers. This team works under the guidance and supervision of editor-in-chief Mr Rakesh Bhargava.

The Research and Editorial Team is responsible for developing reliable and accurate content for the readers. The team follows the six-sigma approach to achieve the benchmark of zero error in its publications and research platforms. The team ensures that the following publication guidelines are thoroughly followed while developing the content:

- The statutory material is obtained only from the authorized and reliable sources

- All the latest developments in the judicial and legislative fields are covered

- Prepare the analytical write-ups on current, controversial, and important issues to help the readers to understand the concept and its implications

- Every content published by Taxmann is complete, accurate and lucid

- All evidence-based statements are supported with proper reference to Section, Circular No., Notification No. or citations

- The golden rules of grammar, style and consistency are thoroughly followed

- Font and size that’s easy to read and remain consistent across all imprint and digital publications are applied