[Opinion] Interplay of ICDS | Ind AS Borrowing Cost

- Blog|News|Account & Audit|

- 2 Min Read

- By Taxmann

- |

- Last Updated on 2 January, 2024

Latest from Taxmann

CA Mohit Manav Sharma & Naman Jhanwar – [2023] 157 taxmann.com 716 (Article)

1. Introduction

- During filing of Tax Audit Report (“TAR”) and Return of Income (“ROI”), taxpayers are found sailing through various Indian Accounting Standards (“IND AS”) and their corresponding Income Computation and Disclosure Standards (“ICDS”).

- Resultantly, taxpayers are facing hardships as to how to synchronize impacts of Ind AS adjustments vis-à-vis Income Tax Act, 1961 (“ITA”).

- In the ensuing paragraphs, we would be analysing, what issues has been dealt in relation to ‘Borrowing Cost’ vide ‘IND AS 23’ and ‘ICDS IX’ respectively and how we should deal under ITA on the respective matters.

Glossary

- Borrowing Cost

Ind AS 23 & ICDS IX: Borrowing cost are the interest and other costs that an entity occurs in connection with the borrowings of funds.

- Qualifying Asset

Ind AS 23 "Qualifying asset is an asset, that necessarily take a "substantial period of time" to get ready for its intended use or sale". Exclusions from Qualifying Asset: - Financial Assets including inventories that are manufactured or otherwise produced over short period of time, are not qualifying assets. - Moreover, assets which are measured at Fair Value and inventories that are manufactured or produced in lots are also not qualifying assets. Note - It is to be noted that borrowing costs shall be capitalized only, if the qualifying asset gives "future economic benefits" & can be "measured reliably".

ICDS IX It includes - Land, building, plant & machinery, etc. (tangible assets) - Know-how, patents, copyrights, etc. (intangible assets) - Inventory manufactured/produced in 12 or more months.

- Substantial Period of Time

Ind AS 23 "Substantial period of time" is subjective in nature. Ordinarily substantial period of time is considered for a period of 12 months, which may differ depending upon the nature of asset obtained from borrowing cost.

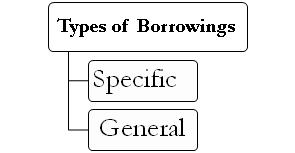

- Specific Borrowing Costs

Ind AS 23 & ICDS IX: Under both the frameworks, specific borrowings refers tothe borrowing cost directly attributable to the acquisition, construction or production of a qualifying asset which shall be the actual cost incurred in obtaining such asset. IND AS 23 provides eligibility to deduct the income earned from the temporary investment of borrowed funds taken specially for obtaining the qualifying asset.

- General Borrowing Costs

IND AS 23 Under IND AS 23, the entity shall determine the amount of borrowing costs eligible for capitalization by applying the capitalization rate to the cost of the asset. The capitalization rate shall be weighted average of the borrowing costs applicable to all the borrowings of the entity that are outstanding during the period. However, specific borrowings shall be excluded from this calculation. ICDS IX According to ICDS IX, the amount of borrowing costs to be capitalized shall be computed by taking the proportion of average cost of qualifying asset and average total cost of asset appearing in balance sheet.

Click Here To Read The Full Article

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.

Taxmann Publications has a dedicated in-house Research & Editorial Team. This team consists of a team of Chartered Accountants, Company Secretaries, and Lawyers. This team works under the guidance and supervision of editor-in-chief Mr Rakesh Bhargava.

The Research and Editorial Team is responsible for developing reliable and accurate content for the readers. The team follows the six-sigma approach to achieve the benchmark of zero error in its publications and research platforms. The team ensures that the following publication guidelines are thoroughly followed while developing the content:

- The statutory material is obtained only from the authorized and reliable sources

- All the latest developments in the judicial and legislative fields are covered

- Prepare the analytical write-ups on current, controversial, and important issues to help the readers to understand the concept and its implications

- Every content published by Taxmann is complete, accurate and lucid

- All evidence-based statements are supported with proper reference to Section, Circular No., Notification No. or citations

- The golden rules of grammar, style and consistency are thoroughly followed

- Font and size that’s easy to read and remain consistent across all imprint and digital publications are applied