Guide to ESG in India – Features | Principles | Reporting Requirements

- Other Laws|Blog|

- 15 Min Read

- By Taxmann

- |

- Last Updated on 6 March, 2024

Latest from Taxmann

Table of Contents

- ESG Evolution in India

- Ten Point Charter

- Voluntary Corporate Social Responsibility Guidelines

- National Voluntary Guidelines

- Business Responsibility Reporting (BRR)

- Transition from NVGs to NGRBC

- National Guidelines on Responsible Business Conduct (NGRBC)

- Changes between NVG & NGRBC

- Key Features of NGRBC

- Nine Principles of NGRBC

Check out Taxmann's Demystifying ESG which discusses the Environmental-Social-Governance (ESG) framework's essential role in modern business, specifically focusing on the Indian context. It offers in-depth insights into each ESG component, providing practical guidance for various stakeholders. It introduces innovative concepts like the 'New Theory of Responsibility' and the 'Solar System Model of ESG', uniquely blending theoretical understanding with practical applications tailored for the Indian business landscape.

A detailed understanding on each Indian Instrument pertaining to ESG is presented while describing it in the process of evolution only. Key ESG Trends and Issues in Indian Context have also been presented. It is also pertinent to understand that when we consider evolution of ESG in Indian Context, we study among others:

- National Voluntary Guidelines on Social, Environmental, and Economic Responsibilities of Business (NVGs), 2011

- Business Responsibility Report (BRR), 2012

- National Guidelines on Responsible Business Conduct (NGRBC), 2019

- Business Responsibility and Sustainability Reporting (BRSR)

- BRSR CORE and LITE Versions.

1. ESG Evolution in India

The National Voluntary Guidelines on Social, Environmental, and Economic Responsibilities of Business (NVGs) were published in 2011 by the Ministry of Corporate Affairs, Government of India. It offered guidance to companies on what constituted ethical business behaviour. SEBI brought out the Business Responsibility Report (BRR) requirement in 2012 which was on disclosures on responsible business, to be done based on the NVGs. Following global developments, the NVGs were revised in 2018 in order to bring them in line with the Sustainable Development Goals (SDGs), the United Nations Guiding Principles on Business & Human Rights (UNGPs), as well as the emerging global issues. Hence, NVGs were revised and new guidelines were released namely, National Guidelines on Responsible Business Conduct (NGRBC) in 2019 following extensive stakeholder con- sultations. The NGBRC was developed to help companies adopt the concept of responsible behaviour beyond the requirements of regulatory compliance.

A Committee on Business Responsibility was constituted for finalising Business Responsibility Reporting formats for listed and unlisted companies. Report of this Committee recommended that BRR be updated to BRSR. Based on the NGRBC and report of the Committee on Business Responsibility Reporting, SEBI notified the BRSR format. The disclosures as per the BRSR framework were made mandatory for the top 1000 listed companies (by market capitalisation) in India from FY 2022-23, while the disclosures were voluntary for FY 2021-22 for these companies.

SEBI has also introduced the ‘BRSR Lite Framework’ for unlisted companies, which covers the essential aspects of ESG reporting for any kind of businesses in country. It is expected that the reporting requirement may be extended by the Ministry of Corporate Affairs to unlisted companies above a specified threshold of turnover or paid-up capital. Further, the Committee recommends that smaller unlisted companies below this threshold may, to begin with, adopt a Lite version of the format, on a voluntary basis.

The BRSR Core framework is a new regulatory framework for enhancing the ESG disclosures by India’s top 1,000 listed entities. It was introduced by the Securities and Exchange Board of India (SEBI) on March 29, 2023, as a subset of the wider Business Responsibility and Sustainability Reporting (BRSR) framework that SEBI had launched in May 2021. The Gazetted notification came on 12 July 2023 and it prescribes the disclosure and assurance requirements for BRSR Core ESG disclosures for value chain, and assurance requirements. Now listed companies are also expected to mandatorily undertake Reasonable Assurance of BRSR Core, it has been notified that 150 top companies will undertake in FY 23-24, 250 in 24-25,

500 in 25-26 and 1000 in FY 26-27.

Table: Evolution of Business Responsibility Frameworks in India

| Year | Initiative |

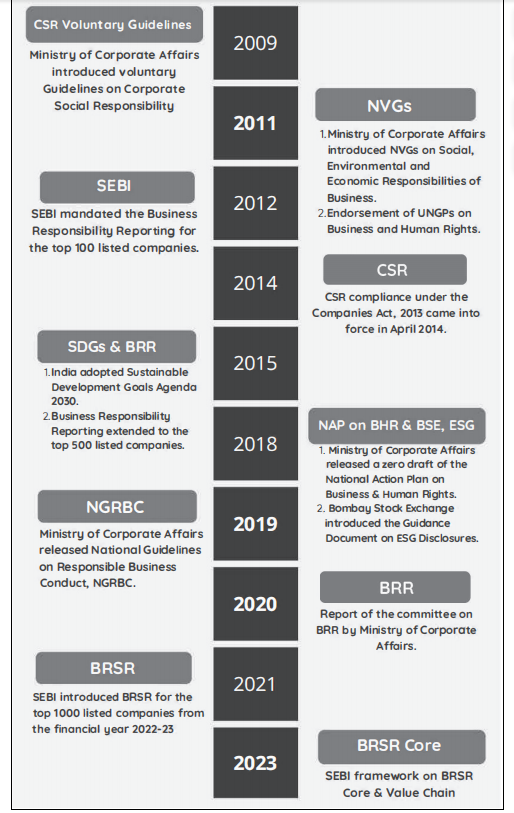

| 2007 | Ten Points Charter by the Hon’ble Prime Minister; |

| 2009 | Voluntary Corporate Social Responsibility Guidelines; |

| 2011 | Endorsement of United Nations Guiding Principles on Business & Human Rights by India; |

| 2011 | Ministry of Corporate Affairs issued National Voluntary Guidelines (NVGs) on Social, Environmental and Economic responsibilities of Business; |

| 2012 | SEBI mandates top 100 listed companies by market capitalization to file Business Responsibility Reports (BRR) based on NVGs; |

| 2014 | Introduction of the CSR Provisions in the Companies Act, 2013; |

| 2015 | SEBI extends BRR reporting to top 500 companies by market capitalization; |

| 2019 | Ministry of Corporate Affairs released the National Guidelines on Responsible Business Conduct (NGRBC). |

2. Ten Point Charter

In May 2007, the then Prime Minister of India, Shri Manmohan Singh, proposed a Ten Point Charter for Business that included: the inclusive employment and humane treatment of workers, investments in communities, ethical practices in all business dealings, investments in environment-friendly practices and technology, promotion of socially-responsible media and advertising, responsible consumption, and promotion of enterprise and innovation. This was in response to contemporary media and civil society reports of high-profile cases of social, environmental and economic violations by businesses and the resultant negative impacts on different stakeholders and on economic activity. At the same time, business needed to positively contribute more actively to the national goals of inclusive growth and sustainable development.

3. Voluntary Corporate Social Responsibility Guidelines

All the issues in ten point’s charter remained relevant and found place in the voluntary Corporate Social Responsibility Guidelines-released by the Ministry of Corporate Affairs in 2009. The guideline, in its preamble, outlines the context, state that the 21st century is characterised by unprecedented challenges and opportunities arising from globalisation, including the desire for inclusive growth and the imperatives of climate change. The guidelines comprise six core elements:

(a) Care for all stakeholders

(b) Ethical business practice

(c) Respect for Worker’s Rights and Welfare

(d) Respect for Human Rights

(e) Respect for the Environment

(f) Activities for Social and Inclusive Development.

Guidelines Drafting Committee

Based upon stakeholder feedback for a more comprehensive guideline, the Indian Institute of Corporate Affairs (IICA) was tasked by the Ministry of Corporate Affairs to undertake the process of ‘review and elaboration’ of the Guidelines, and a multi-stakeholder Guidelines Drafting Committee (GDC) was constituted in 2009, its mandate was as under:

(a) To formulate a draft framework guideline for social, environmental responsibilities of business, which would be offered to enterprises for voluntary adoption with wide applicability across all enterprises, irrespective of their size, and that the guidelines serve to ultimately enhance the performance of business.

(b) To specifically ensure that the framework addresses the concerns of Inclusive Growth and Sustainability.

Further, the GDC was encouraged to ‘draw insights from good-practices and international norms and frameworks, as well as from national resources in as much as they help to address Indian particularities. In particular, the GDC took cognizance of key international and national resources focussing on business responsibility and sustainability issues which included:

(a) The International Standards Organisation (ISO)’s Corporate Social Responsibility Guideline (ISO 26000), as an example of a voluntary, holistic and certifiable standard

(b) The UN Global Compact, as an example of a UN-sponsored voluntary code for companies

(c) The OECD Guidelines for Multinational Enterprises, as an example of State-sponsored and supported initiative

(d) The Global Reporting Initiative (GRI), as an example of a holistic voluntary disclosure and reporting framework for companies

(e) Bureau of Indian Standards (BIS): IS 16000, as an example of a domestic workplace standard

(f) Department of Public Enterprises- CSR & (Community Development) Guidelines, as an example of state-driven guidelines for community development initiatives by companies in the public sector.

4. National Voluntary Guidelines

Ministry of Corporate Affairs released National Voluntary Guidelines (NVGs) on Social, Environmental and Economic Responsibilities of Business in 2011. NVGs comprise inter-related and inter-connected Nine Principles. Each of the nine Principles is explained through a Brief Description and accompanied by attendant Core Elements. the principles can be broadly aggregated as Social (P3, P4, P5, P8 and P9) Environmental (P2, P6 or Governance (P1 and P7). The Social can be further sub-divided into stakeholder-specific principles (P3, P8 and P9) and cross-cutting ones (P4 and P5).

Principle 1: Businesses should conduct and govern themselves with Ethics, Transparency and Accountability

Principle 2: Business should provide goods and services that are safe and contribute to sustainability throughout their life cycle

Principle 3: Businesses should respect and promote the well-being of all employees

Principle 4: Businesses should respect the interests of, and be responsive towards all its stakeholders, especially those who are disadvantaged, vulnerable and marginalized

Principle 5: Businesses should respect and promote human rights

Principle 6: Businesses should respect, protect, and make efforts to protect and restore the environment

Principle 7: Businesses, when engaged in influencing public and regulatory policy, should do so in a responsible manner

Principle 8: Businesses should support inclusive growth and equitable development

Principle 9: Businesses should engage with and provide value to their customers and consumers in a responsible manner.

(Ministry of Corporate Affairs, 2011)

5. Business Responsibility Reporting (BRR)

Business Responsibility Report (BRR) was introduced in India as part of the Annual Reports for the top 100 listed companies based on market capitalization in 2012. The format of BRR was based on the National Voluntary Guidelines (NVGs) issued by the Ministry of Corporate Affairs. The evolution of Business Responsibility Reporting in India can be traced back to the Corporate Voluntary Guidelines in 2009 and the endorsement of United Nations Guiding Principles on Business & Human Rights by India in 2011. The Committee on Business Responsibility Reporting proposed two formats for disclosures: a comprehensive format and a Lite version is a disclosure of adoption of responsible business practices by a listed company to all its stakeholders. This report is applicable to all types of companies including manufacturing, services, etc. The report is important considering the fact that these companies have accessed funds from the public, have an element of public interest involved, and are obligated to make exhaustive disclosures on a regular basis.

6. Transition from NVGs to NGRBC

The Ministry of Corporate Affairs (MCA), Government of India, released a set of guidelines in 2011 called the National Voluntary Guidelines on the Social, Environmental and Economic Responsibilities of Business (NVGs). This was expected to provide guidance to businesses on what constitutes re- sponsible business conduct. In order to align the NVGs with the Sustainable Development Goals (SDGs) and the ‘Respect’ pillar of the United Nations Guiding Principles (UNGP) the process of revision of NVGs was started in 2015. After, revision and updation, the new principles are called the National Guidelines on Responsible Business Conduct (NGRBC). As with the NVGs, the NGRBC has been designed to assist businesses to perform above and beyond the requirements of regulatory compliance.

In 2017, Ministry of Corporate Affairs took a considered view, that given the various significant international and national developments had taken place related to the business responsibility domain and since sufficient time had elapsed since the NVGs were released 2011, the NVGs should be updated to include such developments, which may include: the UNGPs, the UN SDGs, Paris Agreement on Climate Change, Ratification in 2017 of ILO Core Conventions 138 and 182 on child labour, SEBI’s 2012 notification for Annual BR Reports and the Ministry of Corporate Affairs’ notification in the Companies Act, 2013 mandating companies to undertake CSR among others. Emerging global risks in respect of ESG were also considered. Accordingly, the review exercises and multi-stakeholders consultations were organized throughout the country and comments were sought from public and stakeholders. After considering due processes, the National Guidelines for Responsible Business Conduct (NGRBC) came into shape as an update/new version to the NVGs.

The primary rationale for the update is to capture key national and international developments in the sustainable development agenda and business responsibility field that have occurred since the release of the NVGs in 2011. Some of the key drivers behind the emergence of NGRBC are listed below:

- Core Conventions 138 and 182 on Child Labour by the International Labour Organization (ILO)

- SEBI Annual Business Responsibility Reports (ABRRs)

- Section 135 of the Companies Act, 2013

- The UN Guiding Principles for Business and Human Rights (UNGPs)

- UN Sustainable Development Goals (SDGs)

- Paris Agreement on Climate Change (2015).

The NGRBC are designed to be used by all businesses, irrespective of their ownership, size, sector, structure or location. It is expected that all businesses investing or operating in India, including foreign multinational corporations (MNCs) will follow these guidelines. Furthermore, the NGRBC reiterate the need to encourage businesses to ensure that not only do they follow these guidelines in business contexts directly within their control or influence, but that they also encourage and support their suppliers, vendors, distributors, partners and other collaborators to follow them.

7. National Guidelines on Responsible Business Conduct (NGRBC)

Government of India launched National Voluntary Guidelines on Economic, Social and Environmental Responsibilities of Business in 2007 which were revised in 2009 and 2011. The next revision was introduced as the National Guidelines on Responsible Business Conduct of Business, replacing the earlier guidelines. (Ministry of Corporate Affairs, Govt. of India, 2018).

Nine principles for performance disclosures are:

(a) Ethical, Transparent and Accountable conduct

(b) Provide goods and services in sustainable and safe way

(c) Promote the well-being of all employees including those in value chain

(d) Respect the interests of all shareholders

(e) Promote human rights

(f) Protect and restore the environment

(g) Transparent engagement in public policy

(h) Inclusive growth and equitable development

(i) Provide value to their consumers responsibly

(Ministry of Corporate Affairs, 2019)

A notion about the NGRBC among the readers may be that NGRBC is a business responsibility reporting tool. No doubt that NGRBC provide a framework of reporting also but it is not its mere function. NGRBC is a step by step guide for adopting responsible business conduct by a business. The NGRBC are designed to be used by all businesses, irrespective of their ownership, size, sector, structure or location. It is expected that all businesses investing or operating in India, including foreign multinational corporations (MNCs) will follow these guidelines. Correspondingly, the NGRBC also provide a useful framework for guiding Indian MNCs in their overseas operations, in addition to aligning with applicable local national standards and norms governing responsible business conduct.

Considering the national and international developments in the domain of RBC, the nine principles of NVGs have been modified and words such as sustainable, integrity, and respect were included in NGRBCs. This highlights the MoCA commitment towards the advancement of RBC. While NVGs had 48 Core Elements in the updated NGRBC there are 53 Core Elements.

8. Changes between NVG & NGRBC

An overview of modifications is presented in the table below:

| NGRBC 2019 | NVG 2011 | |

| 1. | Businesses should conduct and govern themselves with integrity in a manner that is ethical, transparent and accountable | Businesses should conduct and govern themselves with Ethics, Transparency and Accountability |

| 2. | Businesses should provide goods and services in a manner that is sustainable and safe | Businesses should provide goods and services that are safe and contribute to sustainability throughout their life cycle |

| 3. | Businesses should respect and promote the well-being of all employees, including those in the value chain | Businesses should promote the well being of all employees |

| 4. | Businesses should respect the interests of and be responsive to all its stakeholders | Businesses should respect the interests of, and be responsive towards all stakeholders, especially those who are disadvantaged, vulnerable and marginalised |

| 5. | Businesses should respect and promote human rights | Businesses should respect and promote human rights |

| 6. | Businesses should respect and make efforts to protect and restore the environment | Business should respect, protect, and make efforts to restore the environment |

| 7. | Businesses, when engaging in influencing public and regulatory policy, should do so in a manner that is responsible and transparent | Businesses, when engaged in influencing public and regulatory policy, should do so in a responsible manner |

| 8. | Businesses should promote inclusive growth and equitable development | Businesses should support inclusive growth and equitable development |

| 9. | Businesses should engage with and provide value to their consumers in a responsible manner | Businesses should engage with and provide value to their customers and consumers in a responsible manner |

The NGRBC are the framework that companies can use to integrate RBC practices into their operations and strategy in order to keep pace with the rapidly changing business environment and thrive in the uncertain world we live in.

9. Key Features of NGRBC

- The NGRBC consist of two chapters and an expanded set of annexures*

- NGRBC Principles have been updated, but they have retained the articulation and description of NVGs.

- More emphasis on Core elements of the principles

- Practical guidance to businesses to adopt NGRBC

- Practical guidance on implementation of NGRBC

- Business case for MSMEs has been given

- Updated Business Responsibility Reporting (BRR) Framework

- Serves as a tool for the companies to assess company’s initiatives towards responsible business conduct

- Serves as tool to identify opportunities to improve responsible business conduct

- Serves as a framework for regulators to develop disclosure formats.

*The Guidance has following annexure:

- Guidance on adoption of NGRBC

- Guidance for Micro, Small and Medium Enterprises

- Business Responsibility Reporting Framework

- SDGs mapped against NGRBC

- Business Case Matrix

- Guidance for businesses on using BRRF as a self-assessment tool

- Indicative Mapping of Indian Laws and Principles against NGRBC

- Resources and reference list.

10. Nine Principles of NGRBC

Principle 1 – Businesses Should Conduct and Govern Themselves with Integrity, and in a Manner that is Ethical, Transparent and Accountable

This Principle recognizes that ethical behaviour in all operations, functions and processes, is the cornerstone of businesses guiding their governance of economic, social and environmental responsibilities. The Principle emphasizes that disclosures on business decisions and actions that impact stakeholders form the fundamental basis of operationalizing responsible business conduct and should be accessible to all relevant stakeholders. It recognizes that businesses are an integral part of society and that they will hold themselves accountable for the effective adoption, implementation, and the making of disclosures on their performance with respect to the Core Elements of these Guidelines. The Principle further emphasizes that the governance structure of the business should ensure this, in line with SDG 16 i.e. peace, justice, strong institutions. Essential indicators of this principle are based on awareness generation in the value chain and among multi-stakeholders, complaints arise, their disposal and unmet fiscal and social obligations. The leadership indicators support in disclosures and disseminating the disclosures.

Principle 2 – Businesses should provide goods and services in a manner that is sustainable and safe

This Principle recognizes the proposition of SDG 12, that sustainable production and consumption are interrelated, contribute to enhancing the quality of life and towards protecting and preserving earth’s natural resources. The Principle further emphasizes that businesses should focus on safety and resource efficiency in the design and manufacture of their products, and use their products in a manner that creates value while minimizing and mitigating its adverse impacts on the environment and society through all stages of its life cycle, from design to final disposal. Over time, businesses should embrace the idea of circularity in all its operations. In order to do so, the Principle encourages businesses to understand all material sustainability issues across their product life cycle and value chain. The performance disclosure indicators for this principle includes goods and services incorporating environmental and social concerns, risks and opportunities, investment, raw material and processes adopted and impact of products across value chains.

Principle 3 – Businesses should respect and promote the well-being of all employees, including those in their value chains

This Principle encompasses all policies and practices relating to the equity, dignity and well-being, and provision of decent work (as indicated in SDG 8), of all employees engaged within a business or in its value chain, without any discrimination and in a way that promotes diversity. The principle recognizes that the well-being of an employee also includes the well being of her/his family. Some of the Disclosure indicators under this principle are – complaints received and resolved, status of the employee associations, child and forced labour in value chains, wages and wage ratio, harassment and safety at workplace, skill upgradation of employees among others.

Principle 4 – Businesses should respect the interests of and be responsive to all its stakeholders

This Principle recognizes that businesses operate in an eco-system comprising a number of stakeholders, beyond shareholders and investors, and that their activities impact natural resources, habitats, communities and the environment. The Principle acknowledges that it is the responsibility of businesses to ensure that the interests of all stakeholders, especially those who may be vulnerable and marginalized, are protected. The Principle further recognizes that businesses have a responsibility to maximize the positive impacts and minimize and mitigate the adverse impacts of its products, operations, and practices on all their stakeholders. Essential disclosure indicators are related to the list of stakeholder groups, processes, local engagements, frequency of engagement, marginalized groups etc.

Principle 5 – Businesses should respect and promote human rights

This Principle recognizes that human rights are rights inherent to all human beings, and that everyone, individually or collectively, is entitled to these rights, without discrimination. It further recognizes that human rights are inherent, inalienable, interrelated, interdependent and indivisible. The Principle is inspired, informed and guided by the Constitution of India and the International Bill of Rights and recognizes the primacy of the State’s duty to protect and fulfil human rights. The Principle is further informed and guided by the UN Guiding Principles on Business and Human Rights in its articulation of the responsibility of businesses to respect human rights. It affirms that the responsibility of businesses to respect human rights requires that it avoids causing or contributing to adverse human rights impacts, and that it addresses such impacts when they occur. The Principle urges businesses to be especially responsive to such persons, individually or collectively, who are most vulnerable to, or at risk of, such adverse human rights impacts. Some of the indicators in reporting under this principle are – training on human rights, human rights policies and their coverage, stakeholders groups for reporting human rights violations, corrective actions, human rights due diligence etc.

Principle 6 – Businesses should respect and make efforts to protect and restore the environment

This Principle recognizes that environmental responsibility is a prerequisite for sustainable economic growth and for the well-being of society. The Principle emphasizes that environmental issues are interconnected at the local, regional and global levels, which makes it imperative for business- es to address issues like pollution, biodiversity conservation, sustainable use of natural resources and climate change (mitigation, adaptation and resilience) in a just, comprehensive and systematic manner. These are aligned with SDGs 11, 13, 14 and 15. The Principle encourages businesses to assess environment impacts of its products and operations and take steps to minimize and mitigate its adverse impacts where these cannot be avoided. The Principle encourages businesses to adopt environmental practices and processes that minimize or eliminate the adverse impacts of its operations and across the value chain. The Principle encourages businesses to follow the Precautionary Principle in all its actions. Essential disclosure indicators for the principle are – potential risks on environment and good practices in reuse, recycling and reduction the risks, collective action, specific contribution, and creation of new business product/service etc.

Principle 7 – Businesses, when engaging in influencing public and regulatory policy, should do so in a manner that is responsible and transparent

This Principle recognizes that businesses operate within specified national and international legislative and policy frameworks, which guide their

growth and also provide for certain desirable restrictions and boundaries. The Principle recognizes the legitimacy of businesses to engage with governments for redressal of a grievance or for influencing public policy. The Principle emphasizes that public policy advocacy must expand public good. Disclosures related to the affiliations with trade bodies, industry associations, political parties, monetary contributions, public policy advocacy positions, and corrective actions related indicators are done.

Principle 8 – Businesses should promote inclusive growth and equitable development

This Principle recognizes the challenges of social and economic development faced by India, and builds upon the national and local development agenda as articulated in government policies and priorities. This is particularly significant in zones affected by social disharmony and low human development. The Principle recognizes the value of the energy and enterprise of businesses and encourages them to innovate and contribute to the overall development of the country with a specific focus on disadvantaged, vulnerable and marginalized communities, as articulated in Section 135 of the Companies Act, 2013. The Principle also emphasizes the need for collaboration amongst businesses, government agencies and civil society in furthering this development agenda in line with SDG 17. The Principle reiterates that business success, inclusive growth and equitable development are interdependent. Disclosure indicators are – social impact of business operations, contribution to vulnerable and marginalized sections of society, relations with local communities, CSR interventions as per the Companies Act, 2013, etc.

Principle 9 – Businesses should engage with and provide value to their consumers in a responsible manner

This Principle is based on the fact that the basic aim of a business entity is to provide goods and services to its consumers that are safe to use, and in a manner that creates value for both. The Principle recognizes that consumers have the freedom of choice in the selection and usage of goods and services, and that the enterprises will strive to make available products that are safe, competitively priced, easy to use and safe to dispose of, for the benefit of their consumers. The Principle also recognizes that businesses should play a key role, along with other relevant stakeholders, in mitigating the adverse impacts that excessive consumption of its products may have on the overall well-being of individuals, society and our planet, in line with SDG 12. Some of the disclosure indicators are – adverse impact of goods or service in public domain, consumer complaints, advertising, delivery, corrective actions, international/national product label and certifications, etc.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.

Taxmann Publications has a dedicated in-house Research & Editorial Team. This team consists of a team of Chartered Accountants, Company Secretaries, and Lawyers. This team works under the guidance and supervision of editor-in-chief Mr Rakesh Bhargava.

The Research and Editorial Team is responsible for developing reliable and accurate content for the readers. The team follows the six-sigma approach to achieve the benchmark of zero error in its publications and research platforms. The team ensures that the following publication guidelines are thoroughly followed while developing the content:

- The statutory material is obtained only from the authorized and reliable sources

- All the latest developments in the judicial and legislative fields are covered

- Prepare the analytical write-ups on current, controversial, and important issues to help the readers to understand the concept and its implications

- Every content published by Taxmann is complete, accurate and lucid

- All evidence-based statements are supported with proper reference to Section, Circular No., Notification No. or citations

- The golden rules of grammar, style and consistency are thoroughly followed

- Font and size that’s easy to read and remain consistent across all imprint and digital publications are applied