International Transaction

- Blog|International Tax|

- 7 Min Read

- By Taxmann

- |

- Last Updated on 22 January, 2021

Latest from Taxmann

%20Title%202019_L.jpg)

What is International Transaction?

Section 92B of the Income-tax Act, 1961 defines the term “international transaction as under: “92B. (1) For the purposes of this section and sections 92, 92C, 92D and 92E, “international transaction” means a transaction between two or more associated enterprises, either or both of whom are non-residents, in the nature of purchase, sale or lease of tangible or intangible property, or provision of services, or lending or borrowing money, or any other transaction having a bearing on the profits, income, losses or assets of such enterprises, and shall include a mutual agreement or arrangement between two or more associated enterprises for the allocation or apportionment of, or any contribution to, any cost or expense incurred or to be incurred in connection with a benefit, service or facility provided or to be provided to any one or more of such enterprises.

Analysis of definition of International Transaction:

The definition of international transaction is an exhaustive one with every transaction entered into between Associated Enterprises being categorized as an international transaction. However, the principle condition to be satisfied for such AE transactions to be termed as an ‘international transaction’ is that at least one of the parties to the transaction should be a non-resident. Example: X Ltd. Is a Japanese Company which has its subsidiary named Y Ltd. In India. Y Ltd. manufactures industrial goods that are sold to its parent Company in Japan. In this case, the transaction of sale of industrial goods by Y Ltd. To X Ltd. Is an international transaction under section 92B(1) since both Company X and Company Y are related parties and one of the two related parties is a non-resident.

Extension in scope of definition through insertion of Explanation to section 92B:

The scope of definition of International transaction has been extended in Finance Act 2012 with retrospective effect from 1st April, 2002. Various international transactions that were earlier outside the scope of transfer pricing have been brought within the ambit of Indian Transfer Pricing regulations through inserting Explanation to section 92B. The expanded definition shall include the following transactions to be defined as international transaction: a. Transactions in the nature of purchase, sale or lease of properties, whether the property involved is tangible or intangible in nature; b. Transactions wherein one party provides services to another; c. Capital Financing transactions which involve both lending and borrowing money for short and long term purposes; d. Transactions involving cost allocation or apportionment between the AEs; e. Business restructuring and reorganization transactions; f. Any other transaction having a bearing on the profits, income, losses or assets of an enterprise.

a. Purchase, Sale or lease of Tangible or Intangible Property:

Tangible property means a property which has a physical form, whereas, intangible property means a property which is devoid of physical characteristics. As per Section 92B(1), transactions in the nature of purchase, sale or lease of tangible or intangible property between AEs shall be considered as international transaction for the purpose of transfer pricing regulations. Explanation to Section 92B has also included various items in the definition of tangible and intangible property, thereby widening its scope.

b. Provision of Services:

The definition of International Transaction as mentioned in Section 92B(1) includes the transaction of provision of services between two or more associated enterprises. Explanation to Section 92B has specifically enhanced the scope through including provision of market research, market development, marketing management, administration, technical service, repairs, design, consultation, agency, scientific research, legal or accounting service within the ambit of ‘provision of services’ with retrospective effect from 1st April 2002.

c. Capital Financing transactions:

It is common for companies in a group to enter into financial transactions such as lending or borrowing of money, providing guarantee, etc. Such transactions have an impact on the profits and losses of the enterprise and therefore, such transactions fall under the definition of international transactions. Explanation to Section 92B further expanded the scope of international transaction to expressly cover a range of capital financing transactions namely guarantee, purchase or sale of marketable securities, or any type of advance, payments or deferred payment or receivable and any other debt.

d. Cost Allocation or Apportionment or Contribution:

In a group structure, usually there are a few entities which provide support services to all the entities of the group and the cost incurred by such entities are reimbursed by other group entities receiving such services. The expanded definition of international transaction includes a mutual agreement or arrangement between two or more associated enterprise for the allocation or apportionment of, or any contribution to, any cost or expense incurred or to be incurred in connection with a benefit, service, facility provided or to be provided to any one or more such enterprises.

e. Business Restructuring or reorganization:

Business restructuring may involve cross border transfer of valuable intangible or substantial renegotiation of existing arrangements. Restructuring can be in the form of organizational change (i.e. change in the ownership structure or management of the group entities) or operational change (i.e. change in functional, asset and risk profile of the group entities). Example- merger of two group entities to form a single entity, conversion of full-fledged manufacturer into a contract manufacturer, conversion of a full-fledged distributor into a low risk distributor, demerger of a business unit of an enterprise with an AE etc.

f. Any other transaction:

The definition of International transaction has been expanded through insertion of Explanation to cover any other transaction having a bearing on the profits, income, losses or assets of an enterprise. Such connotation makes the definition wide enough to include within its ambit any other transaction having any bearing on the profits, income, losses or assets of the taxpayer. Examples of these transactions could be reimbursement transactions or transactions which do not involve any charge (i.e. free of cost services or goods).

%20Title%202019_L.jpg)

Deemed International Transaction:

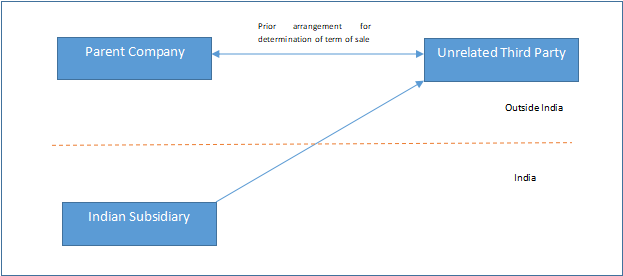

Earlier, associated enterprises used to interpose independent third party in between them and transactions were routed through such unrelated party so that such transaction remains out of transfer pricing provisions. In 2014, a deeming fiction was created in the Indian Transfer pricing regulations wherein the transactions between two unrelated enterprises shall be deemed as international transaction between associated enterprises. There are two preconditions to be fulfilled for considering transaction between unrelated parties to be deemed international transactions namely:

- The existence of a prior agreement in relation to the relevant transaction between such other person and its AE; or

- The terms of the relevant transaction are determined primarily and in substance between such other person and its AE in that prior agreement.

It is pertinent to note that the transaction fulfilling the above two conditions shall be deemed to be an international transaction irrespective of whether the other person is a non-resident or not. Deemed International Transaction with unrelated overseas third party

In the above example, the Indian subsidiary have concluded a transaction with an unrelated third party located outside India. However, the terms of such transactions have been determined in substance by a prior agreement between such unrelated third party and the parent company of the entity. Accordingly, such transactions by Indian taxpayer with unrelated parties shall also be deemed to be an international transaction.

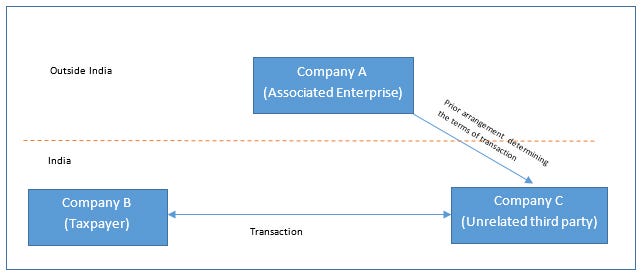

Deemed International Transaction with unrelated domestic third party:

Unlike Section 92B(1) which clearly states that at least one of the parties to international transaction should be a non-resident, Section 92B(2) did not provide any clarification as to whether the unrelated third party with whom the Indian taxpayer transact is required to be a non-resident or not. Subsequently, in order to put litigation on this anomaly to rest, Finance Act, 2014 clarified that even a transaction between a taxpayer with a resident unrelated third party shall be deemed to be an international transaction, if the same is pursuant to a prior arrangement between the third party and non-resident Associated Enterprise. The same can be understood with the help of below diagram.

In the above example, Company A and Company B are AEs. Company B has entered into a transaction with Company C which is a domestic unrelated third party. However, the terms of such transactions have been determined substantially by a prior agreement between Company A (which is a non-resident AE of Company B) and Company C. Before the amendment by Finance Act, 2014 such transactions would have escaped the transfer pricing test. However, after the amendment such transactions are covered within the definition of deemed international transaction and accordingly the same shall be tested for conformity with arm’s length principle.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.

Taxmann Publications has a dedicated in-house Research & Editorial Team. This team consists of a team of Chartered Accountants, Company Secretaries, and Lawyers. This team works under the guidance and supervision of editor-in-chief Mr Rakesh Bhargava.

The Research and Editorial Team is responsible for developing reliable and accurate content for the readers. The team follows the six-sigma approach to achieve the benchmark of zero error in its publications and research platforms. The team ensures that the following publication guidelines are thoroughly followed while developing the content:

- The statutory material is obtained only from the authorized and reliable sources

- All the latest developments in the judicial and legislative fields are covered

- Prepare the analytical write-ups on current, controversial, and important issues to help the readers to understand the concept and its implications

- Every content published by Taxmann is complete, accurate and lucid

- All evidence-based statements are supported with proper reference to Section, Circular No., Notification No. or citations

- The golden rules of grammar, style and consistency are thoroughly followed

- Font and size that’s easy to read and remain consistent across all imprint and digital publications are applied

Comments are closed.